Categories

Mortgage/LenderPublished December 18, 2025

Mortgage Rates Ease After Fed Cut: What It Really Means for Buyers and Homeowners

📉 Mortgage Rates Ease After Fed Cut: What It Really Means for Buyers and Homeowners

Mortgage rates are showing subtle signs of relief following the Federal Reserve’s latest interest rate cut—but the shift isn’t as dramatic as some headlines might suggest. For buyers, homeowners, and anyone watching the housing market closely, understanding why rates are moving (and how they may move next) matters more than the numbers alone.

📊 Where Mortgage Rates Stand Today

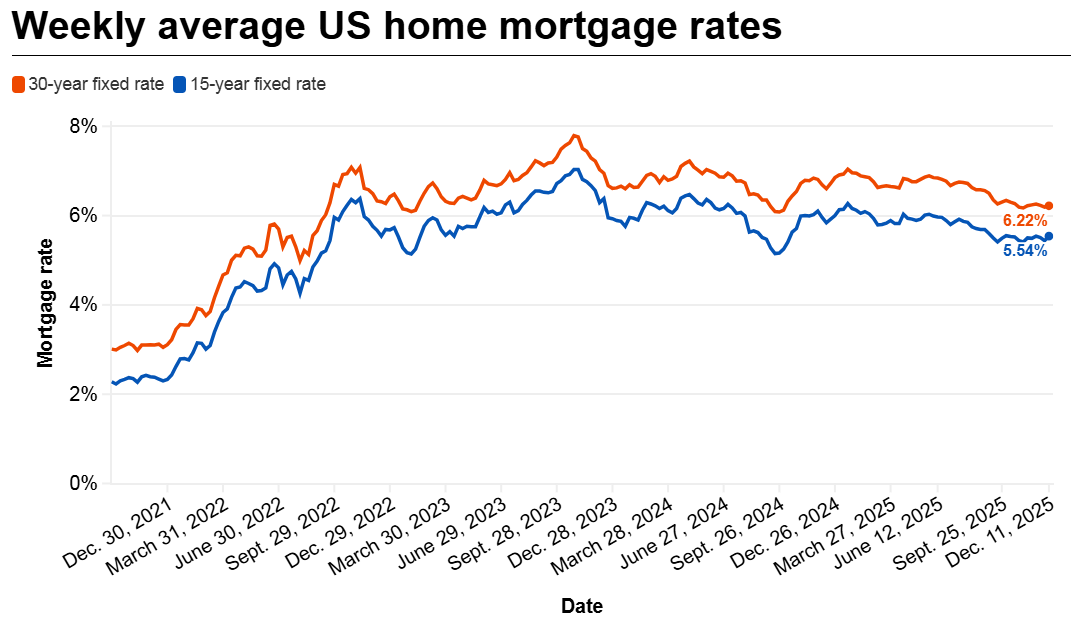

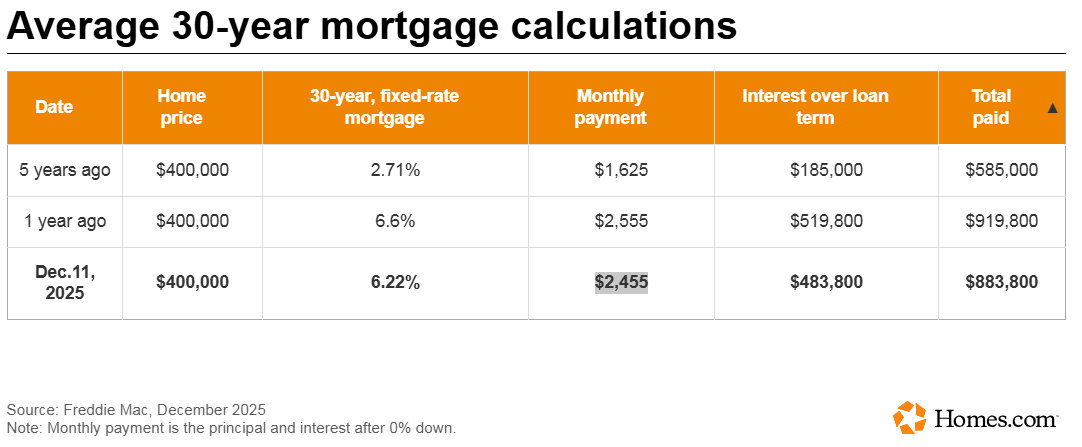

According to Freddie Mac, the 30-year fixed-rate mortgage averaged 6.22% for the week ending Thursday. While that’s slightly higher than the previous week, it remains notably lower than the 6.60% average seen this time last year. Daily data paints a clearer short-term picture: following the Fed’s announcement, daily mortgage rates declined for two consecutive days, with Mortgage News Daily reporting rates around 6.26%.

The 15-year fixed-rate mortgage followed a similar pattern, dipping to 5.76% on a daily basis. Weekly averages rose modestly but remain below year-ago levels.

🏦 Why the Fed Cut Didn’t Cause a Big Drop

A common misconception is that the Federal Reserve directly controls mortgage rates. In reality, the Fed adjusts short-term interest rates, influencing everything from overnight bank lending to broader economic conditions. Mortgage rates respond indirectly—often based on expectations rather than the announcement itself.

This most recent rate cut was widely anticipated. Because markets had already priced it in, there was no sudden or dramatic reaction. As mortgage experts note, when a move is expected, its impact often shows up before the official announcement.

⚖️ A Market Finding Its Balance

Freddie Mac’s chief economist highlighted that borrowing costs are still meaningfully lower than they were earlier this year, helping restore a sense of balance to the housing market. For buyers, that means slightly improved affordability. For sellers, it can translate into steadier demand rather than rapid swings driven by rate volatility.

🔮 What Comes Next for Mortgage Rates?

Looking ahead, the Fed has hinted at the possibility of one rate cut in 2026 and another in 2027—but nothing is guaranteed. Future mortgage rate movement will largely depend on economic data, particularly:

- 🔥 Inflation trends

- 👥 Employment and job growth

- 📉 Signs of economic slowdown or recession

If inflation cools while the job market softens, mortgage rates could trend lower. If inflation rises again and employment remains strong, upward pressure on rates may return.

🏡 What This Means for Buyers and Homeowners

For buyers waiting on the sidelines, today’s environment suggests opportunity—but not perfection. Rates are lower than last year, yet still higher than historic lows. For homeowners, refinancing may start to make sense again for some, especially if rates continue to ease gradually.

Rather than timing the market perfectly, the smartest move is staying informed and prepared. Mortgage rates don’t change overnight—but understanding the forces behind them can help you make confident, well-timed decisions.

As the market continues to adjust, clarity—not speculation—will be the biggest advantage.

Sandie Terenzi

CEO, Broker Associate | Sandie Terenzi | Keller Williams Legacy Partners | PLACE

or another way